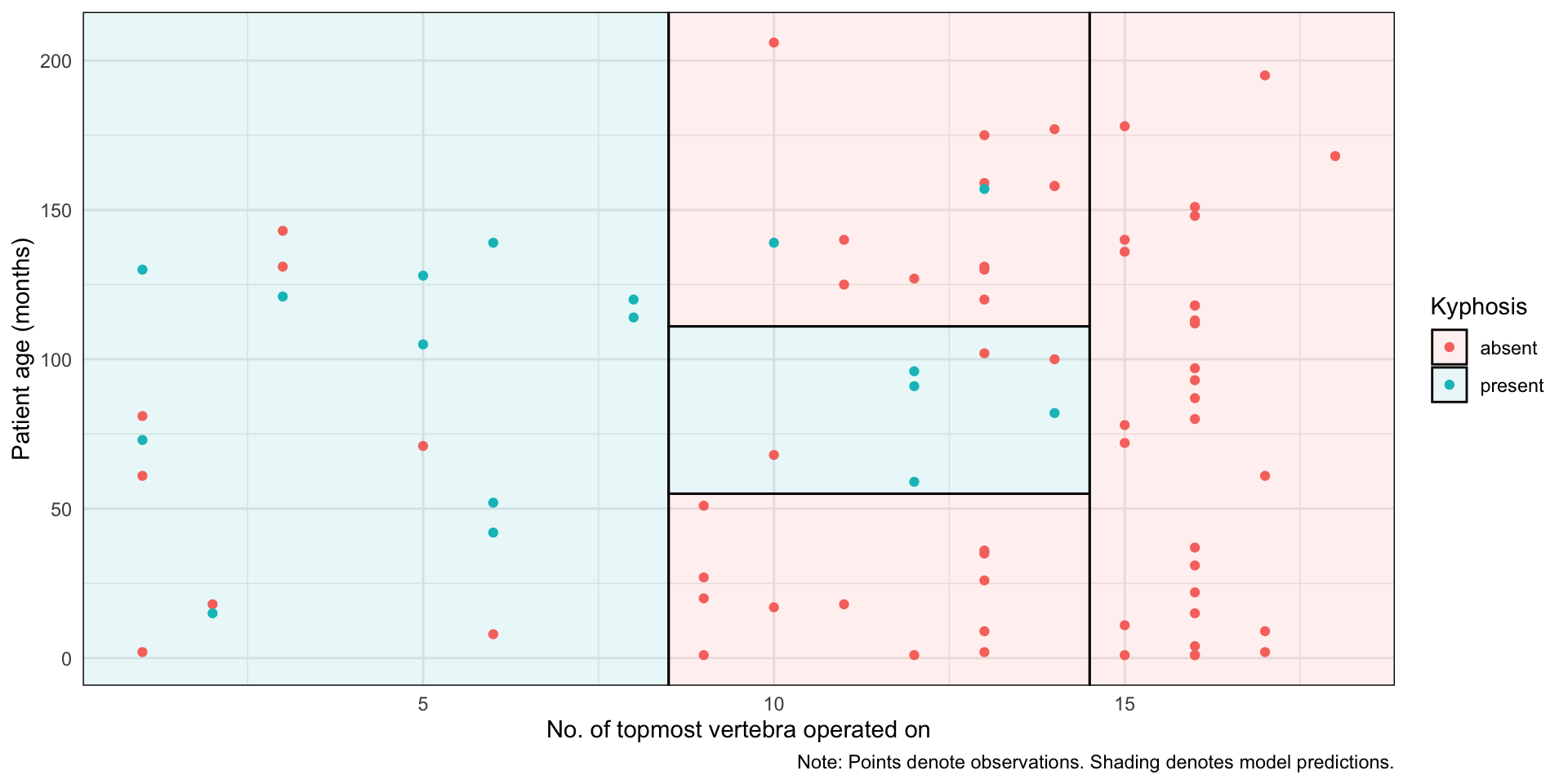

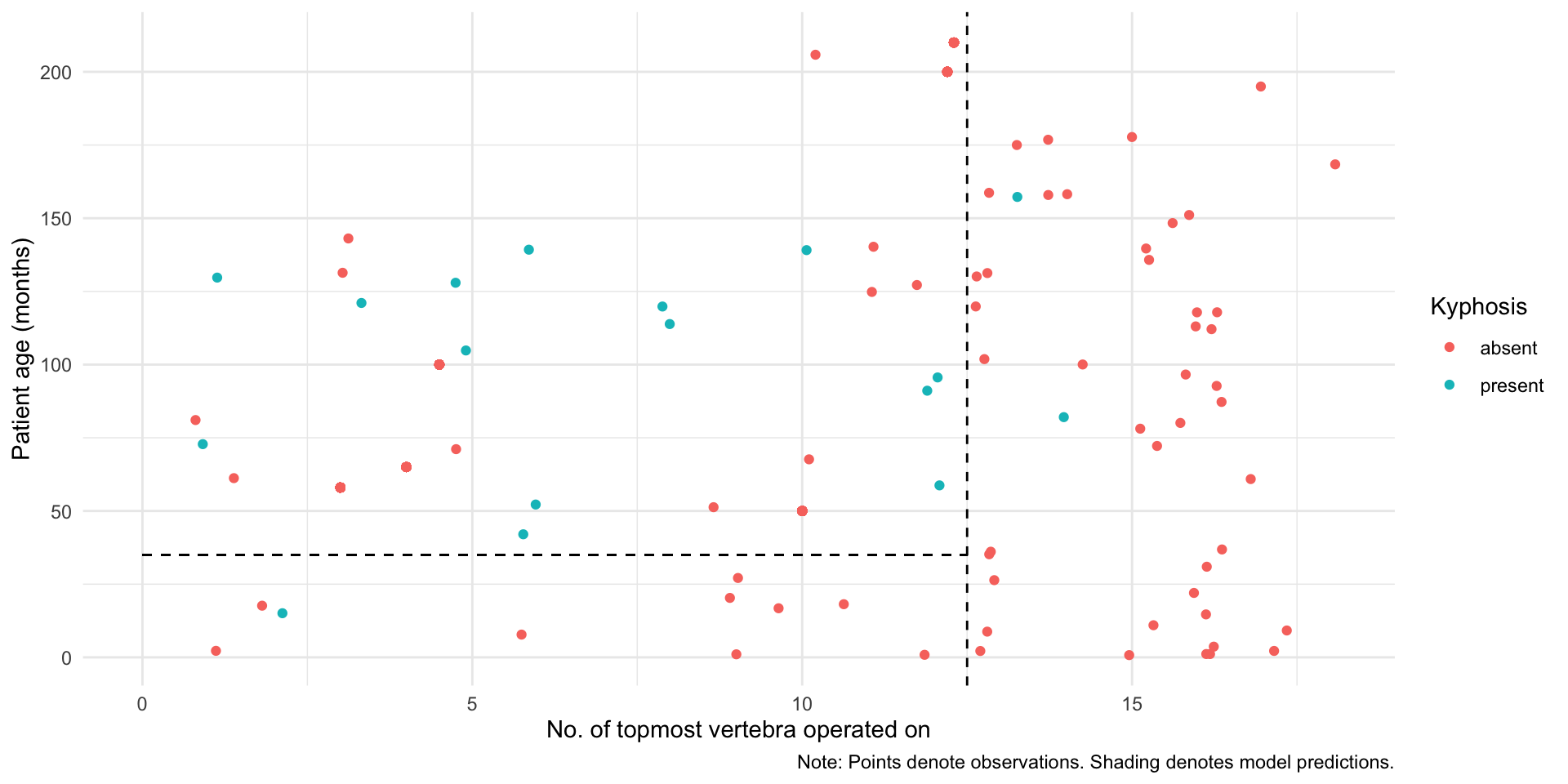

Classification and Regression Trees recursively divide the covariate space into two so that MSE decreases each time we add a partition. In the figure below, we have a partition with 5 leaves.

Code

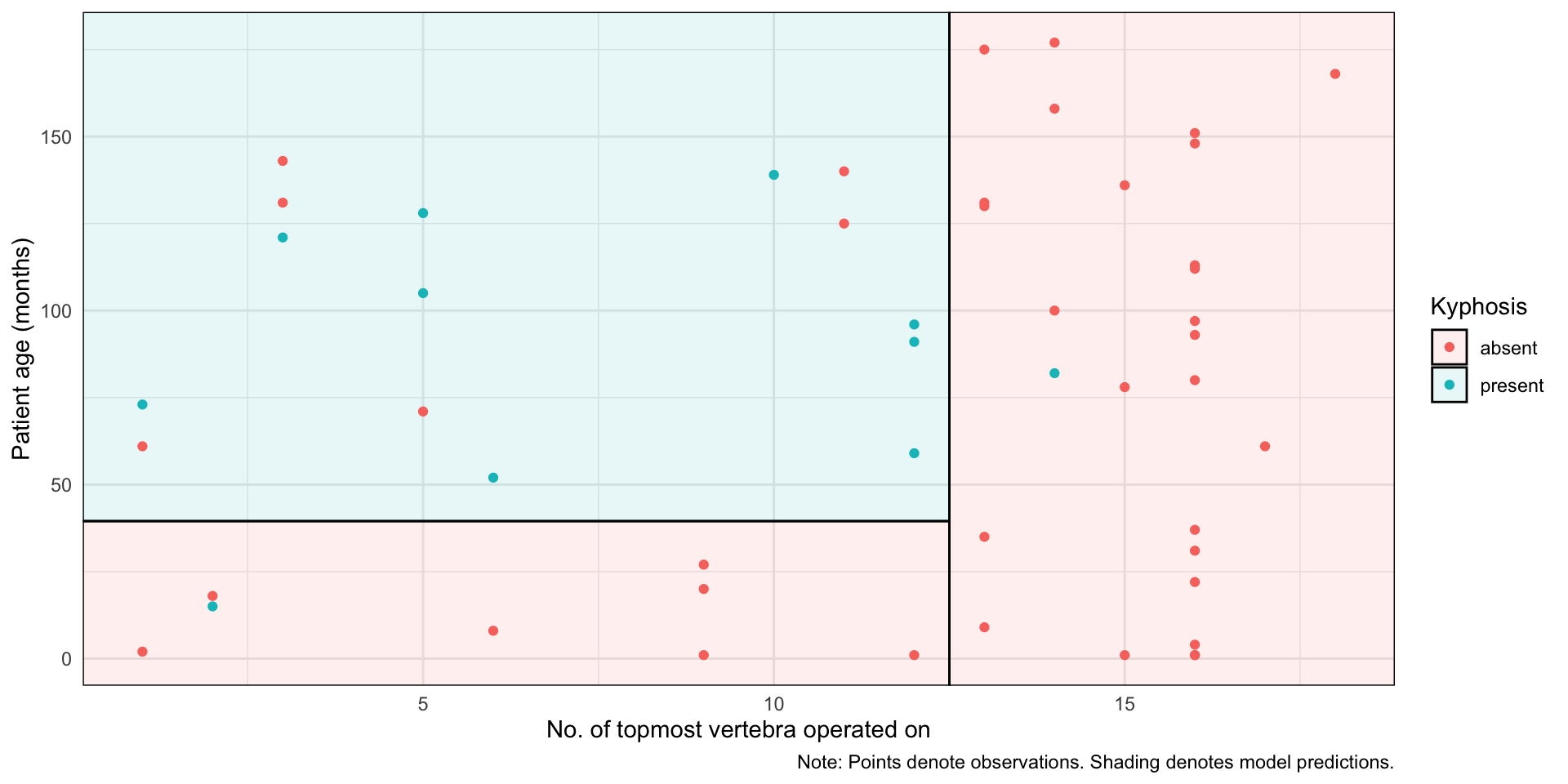

# See the full code at Grant Mcdermott's repositorylibrary(rpart) library(parsnip)library(tidyverse)library(parttree)set.seed(123) ## For consistent jitterfit =rpart(Kyphosis ~ Start + Age, data = kyphosis)ggplot(kyphosis, aes(x = Start, y = Age)) +geom_parttree(data = fit, alpha =0.1, aes(fill = Kyphosis)) +# <-- key layergeom_point(aes(col = Kyphosis)) +labs(x ="No. of topmost vertebra operated on", y ="Patient age (months)",caption ="Note: Points denote observations. Shading denotes model predictions." ) +theme_minimal()

Steps

Choose X_1 or X_2.

Choose the cutoff for dividing.

Repeat these steps.

Trees recursively partition the covariate space so that MSE decreases each time we add a partition.

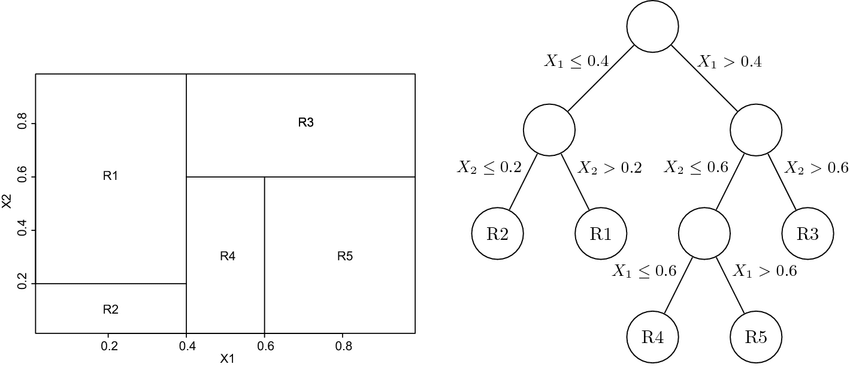

Figure from Beaulac and Rosenthal(2019)

For regression trees, the criterion for choosing covariate and a cutoff pair is the MSE.

Split the data into S^{tr}(training) and S^{te}(test).

Within S^{tr}, choose X_i and a cutoff k that minimizes MSE:

The resulting MSE of the model given a data S and partition \Pi would be

MSE_\mu(S, S^{tr}, \Pi) = \frac{1}{\#(S)} \sum_{i \in S} \biggl[Y_i -\hat{\mu}(X_i; S^{tr}, \Pi)\biggr]^2

In this paper, we use the adjusted MSE:

MSE_\mu(S, S^{tr}, \Pi) = \frac{1}{\#(S)} \sum_{i \in S} \biggl[(Y_i -\hat{\mu}(X_i; S^{tr}, \Pi))^2- {\color{blue}Y_i^2}\biggr]

which does not affect the splitting mechanism but makes the algebra more interpretable.

S^{est} to estimate CATEs and take no role in building a tree

How does this change the tree?

For outcome prediction(Y) - Joonwoo

For CATE(\tau(X)) - Jeongwoo

Simulation Results - Minseo

Honest Inference for Outcome Averages

Notations for predicted outcomes

Given a partition \Pi, conditional mean is given by: \begin{equation*}

\mu(x;\Pi) = \mathbb{E}\left[Y_i | X_i \in \textit{l}(x;\Pi)\right]

\end{equation*}

Given a sample \mathcal{S} we estimate conditional mean is given by \begin{equation*}

\hat{\mu}(x;\mathcal{S},\Pi) = \frac{1}{\#(i \in \mathcal{S} : X_i \in \textit{l}(x;\Pi))}\sum\limits_{i \in \mathcal{S}:X_i \in \textit{l}(x;\Pi)}Y_i

\end{equation*}

Limitations of CART

We cannot simply use CART to estimate HTE.

Potential bias in the leaf estimates

does not consider variance in tree splitting

Limitations of CART

Suppose Y_i \in \mathbb{R}, \quad X_i \in \{L,R\}

Only two possible partitions : \begin{equation*}

\Pi = \begin{cases}

\{L,R\} & (\text{no split}) \\

\{ \{L\}, \{R\} \} & (\text{split})

\end{cases}

\end{equation*}

The second term penalizes a partition that increases variance in leaf estimates (e.g. small leaves) \begin{align*}

-\hat{\mathbb{V}}_{\mathcal{S}^{est},X_i}[\hat{\tau}(X_i;\mathcal{S}^{est},\Pi)]

= -\frac{2}{\text{N}^{\text{tr}}}\sum_{\ell \in \Pi}(\frac{S^2_{\mathcal{S}^\text{tr}_\text{treat}}(\ell)}{p}+\frac{S^2_{\mathcal{S}^\text{tr}_\text{control}}(\ell)}{1-p})

\end{align*}

Pros and Cons of Honest

Pro:

Honest target not only removes potential bias in leaf estimates but also penalizes high variance

Cons: NO reward for heterogeneity of treatment effects

(c.f. \sum\hat{\tau}^2 term in Causal Tree MSE)

Alternative Methods for Constructing Trees

(2) Squared T-statistic Trees (TS)

Su et al., (2009)

Split Rule: split if ({\color{red}\overline{\tau}_L-\overline{\tau}_R})^2 is sufficiently large

similar to two-sample t test

\begin{align*}

T^2 \equiv N \cdot

\frac{({\color{red}\overline{\tau}_L-\overline{\tau}_R})^2}{S^2/N_L+S^2/N_R}

\end{align*} where S^2 is the conditional sample variance given the split

Pros: (only) rewards for heterogeneity of treatment effects

Cons: no value on splits that improve the fit(c.f. Fit-based Trees)

Simulation Study: Set-up

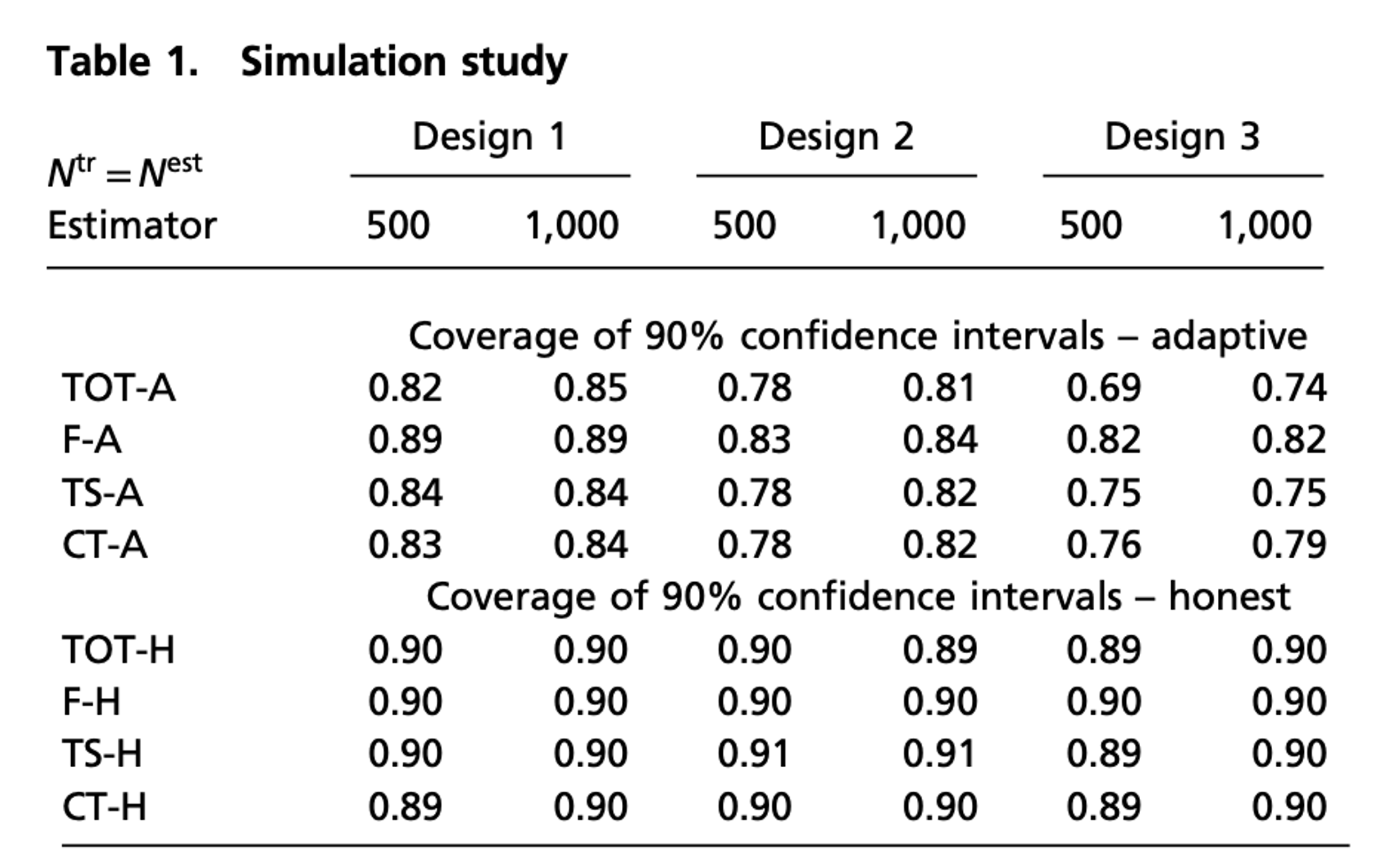

Goal: Compare the performance of proposed algorithms (Adaptive vs. Honest)

Shallower tree (\because smaller leaves \rightarrow higher \mathbb{V})

Smaller # of samples \rightarrow Less personalized predictions and lower MSE

Benefit

EASY

Holding tree from \mathcal{S}^{\color{red}tr} fixed, can use standard methods to conduct inference (confidence interval) within each leaf of the tree on \mathcal{S}^{\color{red}te}

(Disregard of the dimension of covariates)

No assumption on sparsity needed (c.f. nonparametric methods)

vs Dishonest with double the sample

Honest does worse if true model is sparse (also the case where bias is less severe)

Dishonest has similar or better MSE in many cases, but poor coverage of confidence intervals

Use different method (e.g. Radom Forest) to provide a more personalized estimation. Causal Tree is to answer questions on the relation between covariates and how they interplay with treatment effects.

Is smaller number of samples bad?

Again, we’ve moved the goal post here. We are not trying to give the best prediction of effect on individuals. Rather, recursive partitioning assists figuring a general relation between covariates and treatment effects.

Why 50:50 in sample splitting?

Sample ratio could be taken differently in different problems and data available.

Simulation Study: Results

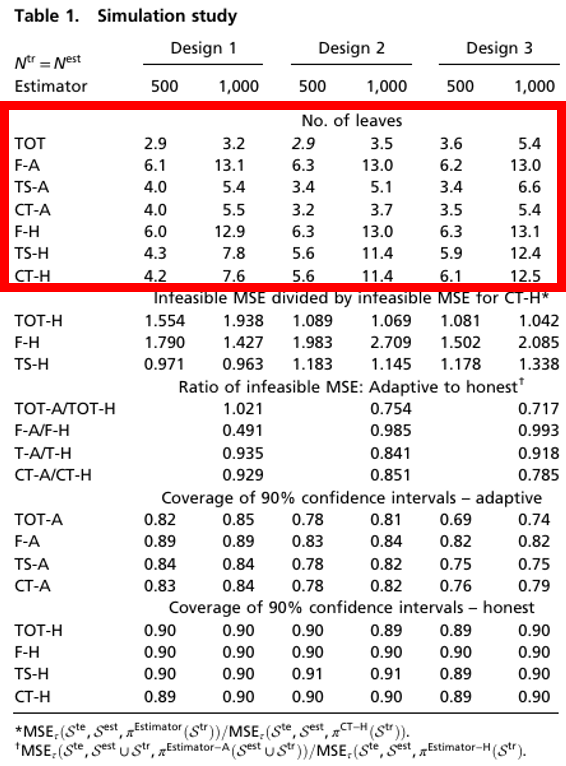

Number of Leaves(Tree Depth)

CT-H:

Splitting criteria: Maximizes – MSE

F-H:

Splitting criteria: Maximizes outcome prediction

Build deeper trees than that of CT

Less prone to overfitting on treatment effects

TS-H:

Splitting criteria: Maximizes squared t-statistic

Tree depth similar to that of CT

Adaptive versions still prone to overfitting

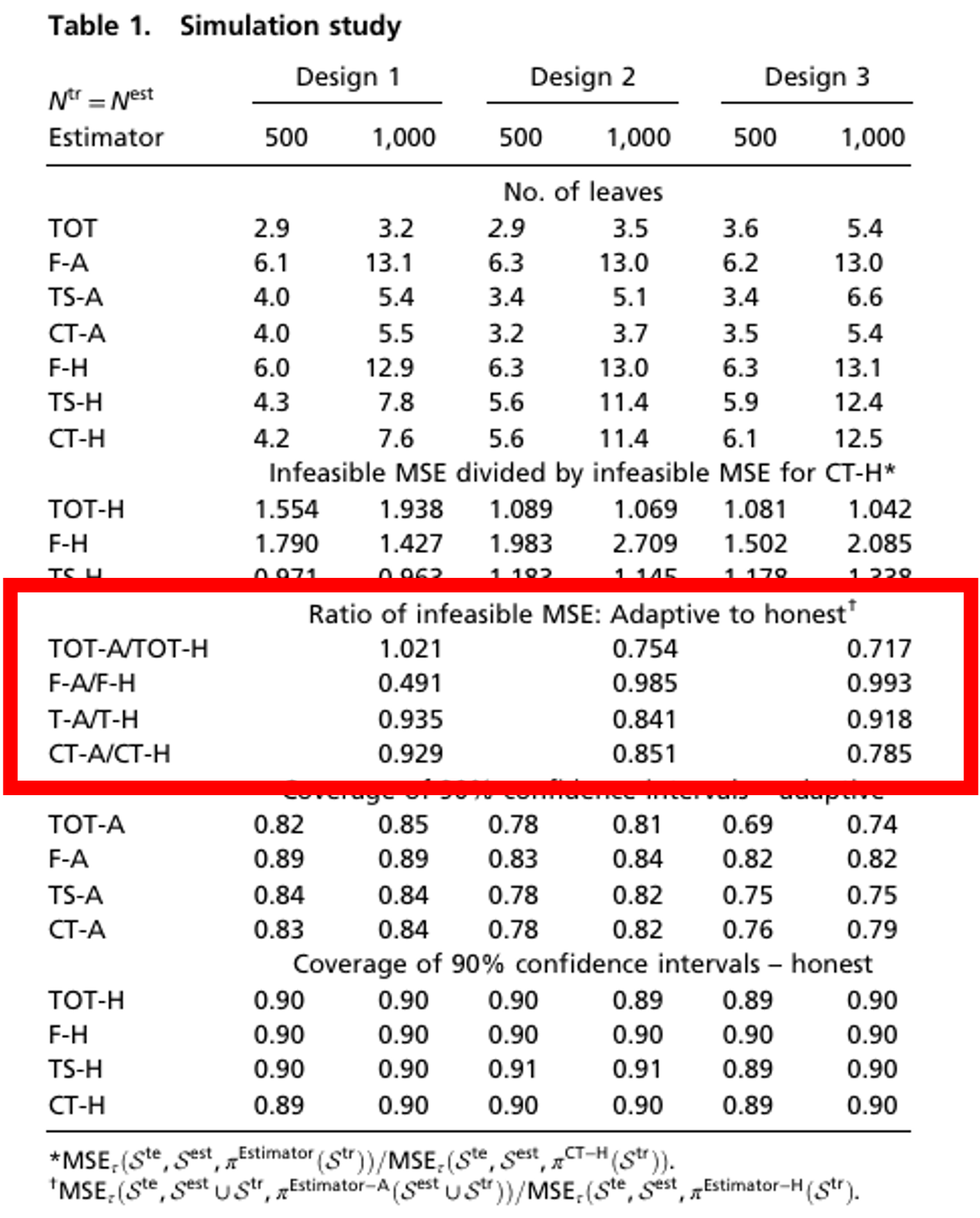

Simulation Study: Results

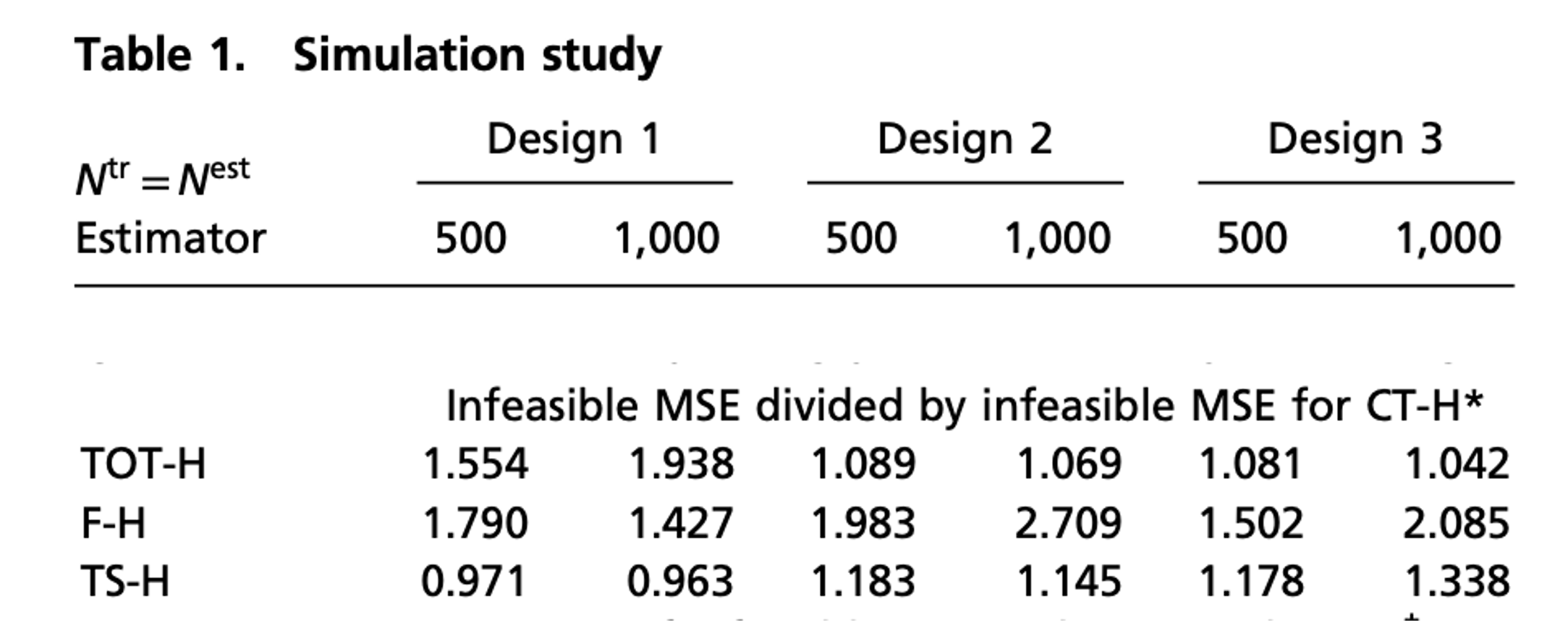

Adaptive vs Honest : Ratio of infeasible MSE

Honest estimation shows higher MSE in most cases \rightarrow Uses only half the data, leading to lower precision

Fit estimator performs poorly in Design 1 \rightarrow With smaller sample size, it tends to ignore treatment heterogeneity

As design complexity increases, the MSE ratio decreases. \rightarrow Adaptive estimators overfit more in complex settings.